What can each sector do to minimise emissions by 2030?

Post Date

06 March 2023

Read Time

7 minutes

This blog post is the fourth in a four-part series unpacking the key pieces of information from the IPCC AR6 reports. Part one - The latest climate science from the IPCC. Part two - Key highlights from the IPCC Impacts, Adaptation and Vulnerability report.Part three- What is required to limit global warming to below 1.5°C-2°C.

The Intergovernmental Panel on Climate Change (IPCC) produces a set of major reports every seven years summarising the latest climate science and its implications for human society. It is currently in its sixth assessment report cycle (AR6).

In April 2022, the IPCC released the third report in the series, AR6 Climate Change 2022: Mitigation of Climate Change. This report, and its various chapters covering energy systems to buildings to industry, looks at the latest science on what is required across human society to decarbonise.

The key highlights are summarised below:

The report states that there are options available now in every sector that can at least halve emissions by 2030. The main options for each sector are summarised below.

There is increased evidence of climate action. For example:

Some countries have achieved a steady decrease in emissions consistent with limiting warming to 2°C.

Zero emissions targets have been adopted by at least 826 cities and 103 regions.

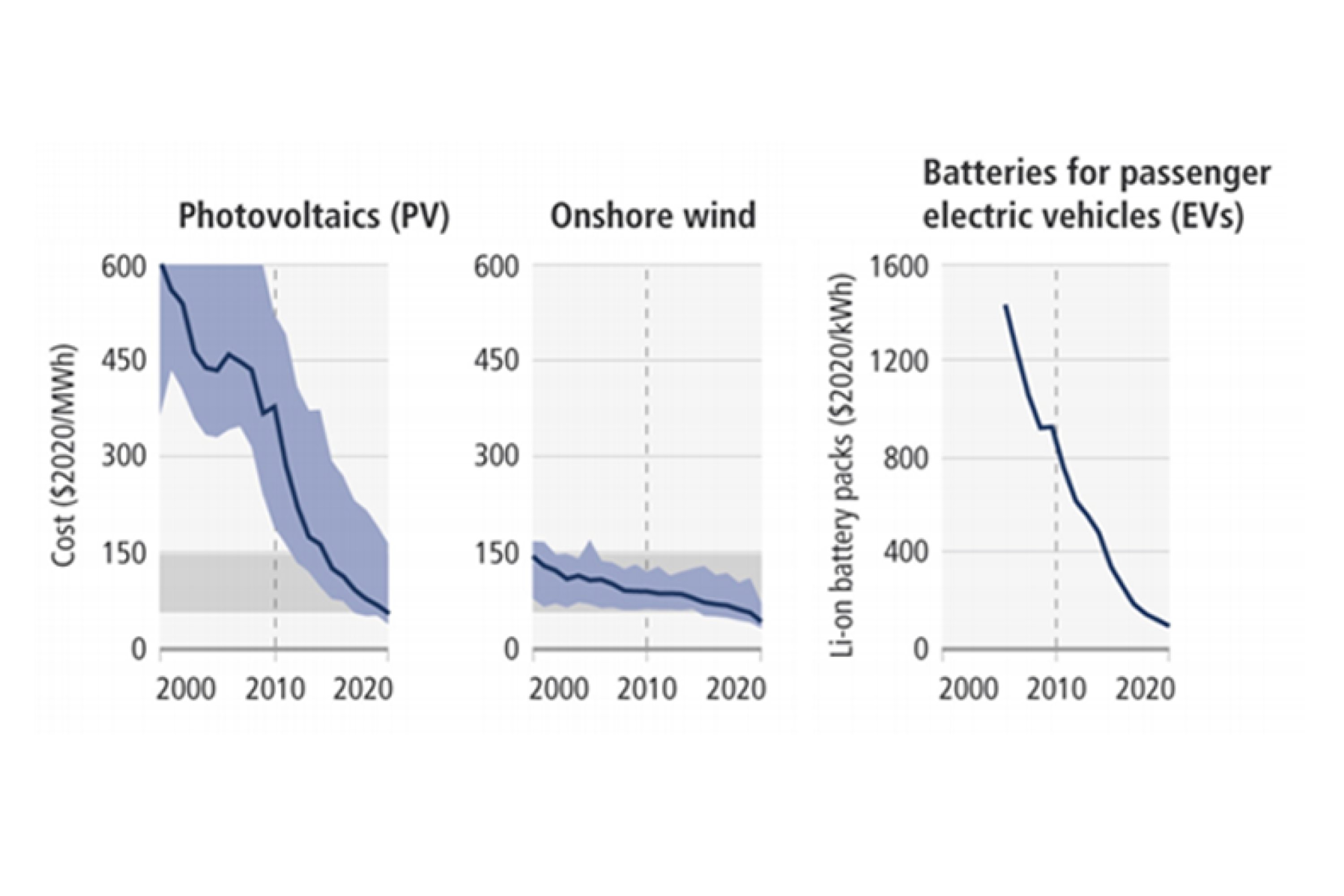

The cost of solar, onshore wind and batteries have declined significantly over the last 20 years.

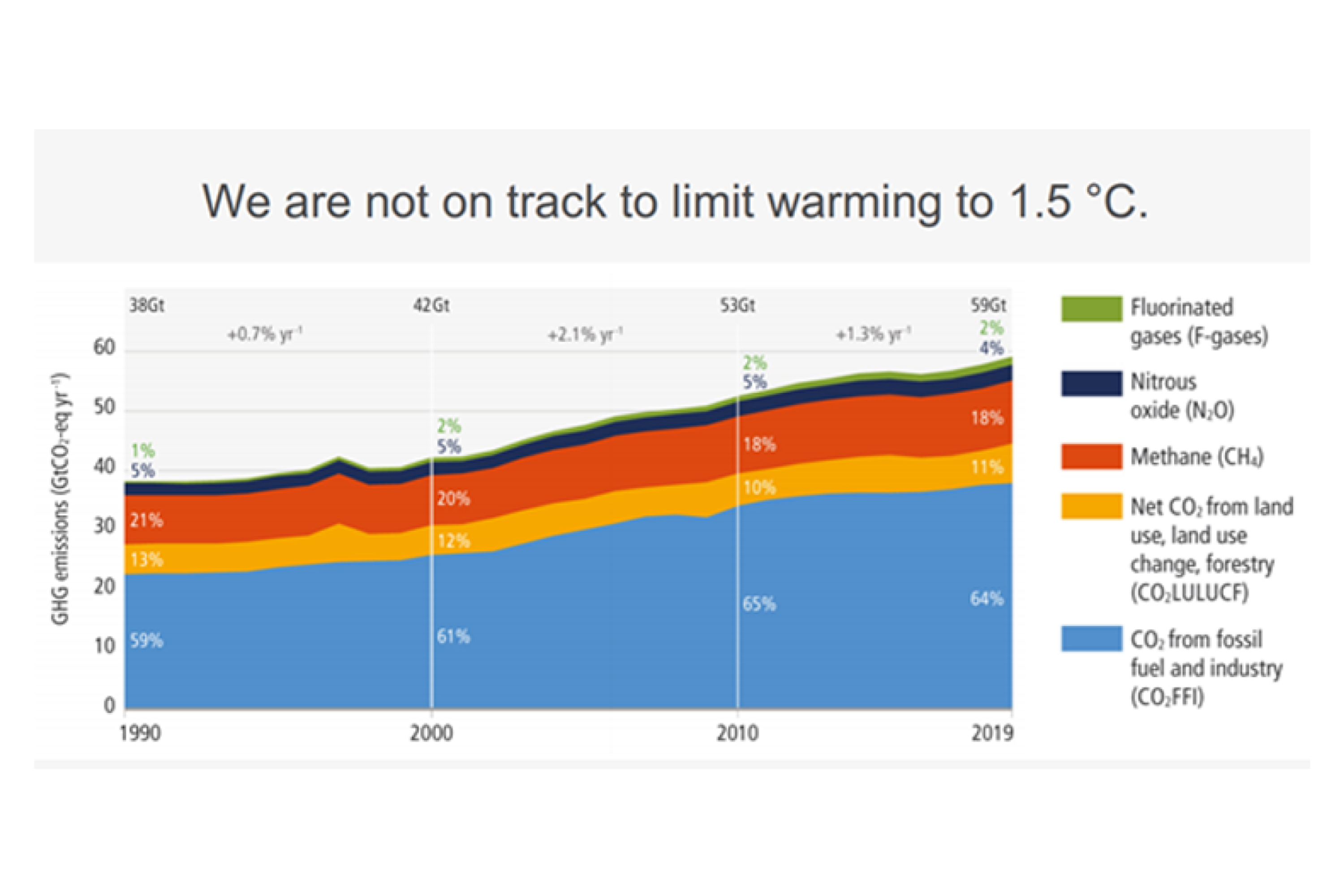

However, the report states that “unless there are immediate and deep emissions reductions across all sectors, 1.5°C is beyond reach”.

Energy

Reduction in fossil fuel use and carbon capture and storage.

Low- or no-carbon energy systems. These systems could entail a mix of variables renewables, dispatchable renewables (e.g., biomass, hydropower), “on-demand” low-carbon generation (e.g., nuclear, CSS-equipped capacity), energy storage, transmission, carbon removal and demand management.

Widespread electrification.

Improved energy efficiency.

Alternative fuels, e.g., hydrogen and sustainable biofuels.

Demand and services

Reduction in demand and shifting services have the potential to bring down global emissions by 40-70% by 2050. This includes moving away from high-emissions activities in wealthy nations such as private road transport, frequent air travel, private jet ownership (for the very wealthy), and meat-intensive diets.

Reduction in transport emissions includes increased walking and cycling, electrified transport, and reducing air travel.

Adapting houses to use less energy can make a large contribution.

Transport

Reducing demand and low-carbon technologies are key to reducing emissions.

Electric vehicles offer the greatest potential for emissions reductions in transport.

Advances in battery technology could enable electric rail and trucking.

Alternative fuels (low emissions hydrogen and sustainable biofuels) are needed for aviation and shipping.

The transport sector has substantial potential for emissions reductions but depends on decarbonising the energy sector.

Cities and urban areas

Improved urban planning, e.g., more green spaces, ponds, trees. These enhance carbon uptake and storage. Examples of the benefits of green roofs and green facades:

Green roofs can reduce building heating demands by about 10–30% compared to conventional roofs, 60–70% compared to black roofs, and 45–60% compared to white roofs.

Green walls or facades can provide a temperature difference between air temperature outside and behind a green wall of up to 10°C, with an average difference of 5°C in Mediterranean contexts in Europe.

The potential of saving energy for air conditioning by green facades can be around 26% in summer months.

Sustainable production and consumption of goods and services, including more local production, for example, increasing urban agriculture. Examples include: urban orchards, roof-top gardens, and vertical farming contribute to enhance food security and fostering healthier diets.

Increasing electrification to benefit from low emissions energy generation.

Buildings

Action is required in the 2020s to reach net zero by 2050.

Zero energy and zero-carbon buildings exist in new builds and retrofits.

Retrofitting existing buildings and implementing effective mitigation techniques in new buildings through ambitious policy packages will be required.

Industry

Using materials more efficiently, reusing, recycling, minimising waste are key.

Policy and practice are not currently encouraging these behaviours to a sufficient degree.

Low- to zero-greenhouse gas production processes are at pilot or near-commercial stage for basic materials. However, achieving net zero will be challenging.

Land use

Sustainable land use can provide large-scale emissions reductions and remove and store CO2 at scale.

Protecting and restoring natural ecosystems to remove carbon. This includes forests, peatlands, coastal wetlands, savannas and grasslands.

Competing demands for land use have to be carefully managed.

The IPCC AR6 is clear to point out that improved land use cannot compensate for delayed emission reductions in other sectors.

Carbon dioxide removal

The IPCC AR6 envisages that CO2 removal will be required to counterbalance hard-to-eliminate emissions and will be essential to achieve net zero.

This can be achieved through biological methods, such as reforestation and soil carbon sequestration.

Non-biological methods require more research, up-front investment, and proof of concept at larger scales.

Agreed methods for measuring, reporting and verification are also required.

Investment and finance

Funding levels are currently insufficient. Levels are 3-6x lower than what is needed by 2030 to limit warming to below 1.5°C or 2°C.

The good news is that there is sufficient global capital and liquidity to close investment gaps.

Challenge of closing gaps is widest for developing countries.

Policies, regulatory and economic instruments

Regulatory and economic instruments have already proven effective in reducing emissions.

Policy packages and economy-wide packages are able to achieve systemic change.

Ambitious and effective mitigation requires coordination across government and society.

Conclusions from this blog series

The latest climate science is deeply concerning. The world is moving rapidly towards 1.5°C, and we can expect this threshold to be breached in the late 2020s to early 2030s. As previous IPCC reports comparing the difference between 1.5°C and 2°C have pointed out, we know that every extra fraction of a degree of warming increases the negative impacts of climate change.

Although there is considerable uncertainty around reinforcing feedback loops, the AR6 series acknowledges these tipping points for the first time, stating that they cannot be ruled out.

The AR6 report series highlights the impacts of climate change on human society, with alarming predictions about the number of people who will be exposed to life threatening heat, and how water scarcity and food security will become increasingly critical issues as warming increases. These issues need to be planned for and acted upon today to limit the severity of their impact, including increasing the level of financing that is directed towards climate adaptation.

The AR6 report series concludes with concrete measures that can be taken in every sector to cut emissions. Many of the technologies required to cut emissions already exist. They now need to be financed, scaled, and widely adopted. There are also common-sense nature-based solutions that can help keep cities cool, such as increasing the amount of green space, including of roof tops and building facades. These are easy wins that city planners and local residents should aim to implement wherever possible.

If ever there was a crucial decade for climate action, the 2020s is it. If not now, when?

Recent posts

Insight

25 March 2026

7 minutes read

China’s first climate disclosure standard officially released: key points companies must know